Inventory cards of fixed assets sample in 1s. Characteristics of the fixed asset accounting card

Accounting for fixed assets owned by the company and moving within its structural divisions should be maintained by issuing a special inventory card.

In accounting, such a card must be entered in one copy, and depending on the number of objects or the type of the enterprise itself, only the form in which it must be drawn up changes.

Dear readers! The article talks about typical ways to solve legal issues, but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FOR FREE!

At the same time, the current legislation in this matter regularly undergoes various changes, and therefore many people do not know how a fixed asset accounting card should be drawn up in 2019 and what its main features are.

Terms and purpose of the document

All issues that are relevant to the conduct are extremely accurately reflected in the current legislation, but in order to correctly understand and interpret the various rules, it is worth considering the basic requirements that they use:

| fixed assets | The main objects that are used directly during the manufacture of products or the gradual receipt of income by the company, while maintaining their natural form. |

| Primary accounting documentation | List of securities reflecting information on various banking operations. Such documents are drawn up immediately at the time of the transaction or any business transaction. |

| The procedure for reflecting data on the financial activities of the company in special tables. | |

| tax accounting | The procedure for reflecting data on the financial activities of the company, on the basis of which the amounts of transfers to the budget are calculated. |

| The gradual transfer of the value of fixed assets to production processes, which is reflected in the relevant reports using an inventory card. |

By itself, maintaining an inventory card allows you to solve a fairly large number of tasks, including:

- simplify the procedure for analyzing data on fixed assets;

- generate statistical data as quickly as possible;

- organize information.

When conducting all kinds of checks, tax authorities always pay special attention to these cards, so the algorithm for filling them out should be studied by authorized employees of the company in as much detail as possible, since if there are errors, a large fine can be imposed on the organization.

Mandatory moments

The registration of an inventory card is subject to certain rules that any authorized person should know, and in particular, this applies not only to the procedure for registration, but also to the content of this document.

Main information in the content

In the OS-6 form, it is necessary to enter data on:

- receipts of fixed assets;

- movements between internal structural divisions;

- repair work;

- modernization or reconstruction of fixed assets;

- revaluation procedures;

- write-off or disposal.

An example of OS-6 form

In the header of the document, you must indicate the full name of the organization, the fixed asset, its location, as well as codes for OKUD, OKOF, and serial number. In addition, the date of acceptance of the fixed assets and their deregistration is also indicated.

The main part of the document includes seven sections-tables, and at the time of acceptance of the object for accounting, the following sections are filled in it:

All other sections should be drawn up already at the time of the direct operation of this facility, and they include the following data:

The completed form must be signed by the responsible person.

If the company has decided to retire fixed assets for one reason or another, then in this case, in accordance with the written-off act, a special mark must be made in the inventory card. At the same time, inventory cards for any retired objects must be kept for the period established by the head of the organization (at least five years).

It should be noted that even if the card was issued in electronic form, after that it will be necessary to draw up a document in written format at the time of carrying out certain operations or upon their completion, if this was not possible before.

How to fill out the fixed assets accounting card

It is worth noting several features that are typical for the procedure for filling out the fixed assets accounting form:

- It is necessary to fill in information about fixed assets at the time of their transfer only if they have already been used before, and entries must be made in accordance with the documents of fixed assets. If we are talking about new equipment, this item is no longer required.

- When filling out information about fixed assets at the time of their acceptance for accounting, only the cost of receiving this object is indicated.

- Revaluation provides for an increase or decrease in the initial cost of the object, and the price that has been changed after that acquires the status of a replacement. In addition, the accrued depreciation is also re-evaluated.

- Information about the acceptance, write-off and movement of fixed assets. Entries are made in order, that is, starting with the data on the receipt of fixed assets. In this section, you need to indicate data on the basis of such documents as acts of acceptance, transfer, write-off and other papers.

- Information about the adjustment of the starting cost of fixed assets is data on the costs necessary for major repairs, adjustments or improvements, which allowed to increase the value of fixed assets. It is indicated on the basis of the data prescribed in the OS-3 form.

- In the expenses for repair work, it is necessary to indicate data on what funds were spent on current repairs that do not affect the cost of the object and are written off to the cost of the product.

- Individual indicators include any information that characterizes an item of fixed assets.

Ultimately, accordingly, the signature should be put by the one who is engaged in the execution of this document and bears full responsibility for it.

Record keeping and billing

For fixed assets, depreciation is charged in the following order:

- on the real estate object at the time of its acceptance for accounting upon the state registration of property rights to the real estate object, provided for by the current legislation;

- for property with a value of less than 40,000 rubles inclusive, depreciation should be calculated as 100% of the total book value of the object at the time of its acceptance for accounting;

- for property having a value of more than 40,000 rubles, depreciation must be charged in accordance with the depreciation rates calculated earlier in the prescribed manner.

If we are talking about movable property, then depreciation on it must be calculated a little differently, namely:

- for library fund objects with a value of less than 40,000 rubles inclusive, depreciation is calculated in the form of 100% of the book value, which was registered at the time the object was put into operation;

- for fixed assets with a value of more than 40,000 rubles, depreciation must be calculated according to accepted depreciation rates;

- for fixed assets, the value of which is less than 3000 rubles inclusive (not counting the objects of the library fund and intangible assets), depreciation cannot be calculated;

- for other items of fixed assets, the value of which is in the range of 3,000-40,000 rubles inclusive, depreciation should be charged in the form of 100% of the book price registered at the time the item was put into operation.

Thus, the rules for calculating depreciation directly depend on the type of property in question and what value it has.

Principles of inventory and storage

Inventory cards of fixed assets belong to the category of primary reporting documents, and therefore they are subject to the usual rules, and in particular, this applies to the duration of storage of documentation - at least five years. After this period of time has elapsed, the documents must be disposed of in the prescribed manner.

This rule also applies to any fixed asset inventory cards, but in some cases, the storage period may be slightly longer, and everything here depends on the type of fixed assets.

Be sure to conduct an inventory of inventory cards every few years, the main purpose of which is to register inventory cards. By carrying out this procedure, confirmation of the safety of all available documentation is ensured, and registration must be carried out without fail in full accordance with the information specified in the budget accounts.

It is necessary to apply, because. all the details of contracts, books and accounts need to be adjusted.

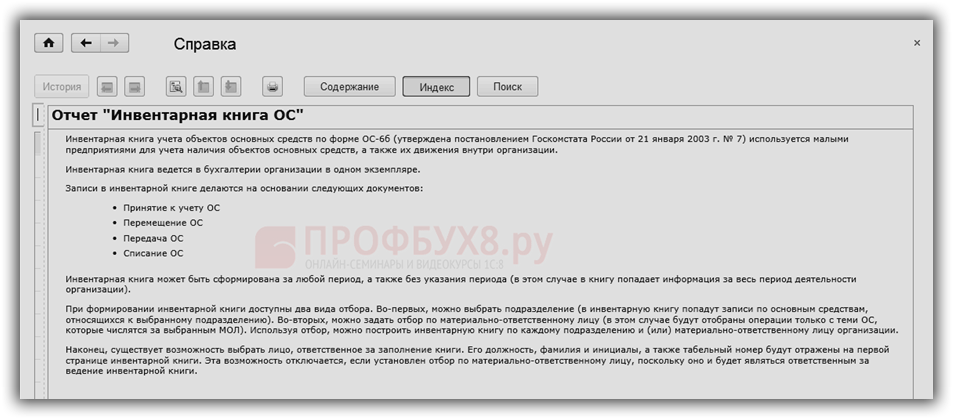

The inventory book must be kept in one copy.

How to create an inventory book in 1C 8.3

In 1C 8.3 with OSNO and USN You can find the inventory card as follows: on the sections panel, select the OS and NMA section, then select the Reports subsection and go to the Inventory book report (OS-6 b):

Open the selected report, click the Generate button:

A sample of filling out an inventory book in the form of No. OS-6 b in 1C 8.3:

Sections of the Inventory Book, which reflect:

- Name of OS object;

- His inventory number;

- Date ;

- Booking date. accounting;

- Structural subdivision;

- Responsible person;

- The initial cost of the OS;

- Useful life of OS;

- Amount of accrued depreciation:

- Residual value of fixed assets;

- OS revaluation;

- Internal relocation, disposal, decommissioning of fixed assets:

Full instructions on how to correctly fill out and draw up the Inventory Book in 1C 8.3 can be found in the same report. To do this, use the More button. When this button is pressed, an additional menu opens with functions, when selected, you can add, change the report plate itself in order to make it convenient to work with it.

So, select the Help function:

We open it and get instructions for creating an inventory book:

There are two ways to create an inventory book in 1C 8.3. To do this, open the Select settings button on the report panel:

Select a specific department:

Indicate the person who is financially responsible for this unit for the safety of the fixed assets:

We form an inventory book for the desired period (month, quarter, year):

There is another possibility of filling out the inventory book in 1C 8.3 - choosing the person who is responsible for the information in this book:

All personal data of the person (full name), personnel number are recorded on the title page of the inventory book:

In order not to perform the Select settings function each time, there is a function in this report - Save settings. We select the required setting and with the Save button we fix the desired setting in 1C 8.3:

You can study the features of reflecting operations for accounting for fixed assets in 1C 8.3 (basic documents, accounting accounts, cost formation and depreciation in accounting records and accounting records) on the module.

When the fixed asset is put into operation, an inventory number must be assigned. What are the nuances, see our video tutorial:

Rate this article:

The inventory book must be kept in one copy.

How to create an inventory book in 1C 8.3

In 1C 8.3 with OSNO and USN You can find the inventory card as follows: on the sections panel, select the OS and NMA section, then select the Reports subsection and go to the Inventory book report (OS-6 b):

Open the selected report, click the Generate button:

A sample of filling out an inventory book in the form of No. OS-6 b in 1C 8.3:

Sections of the Inventory Book, which reflect:

- Name of OS object;

- His inventory number;

- Date ;

- Booking date. accounting;

- Structural subdivision;

- Responsible person;

- The initial cost of the OS;

- Useful life of OS;

- Amount of accrued depreciation:

- Residual value of fixed assets;

- OS revaluation;

- Internal relocation, disposal, decommissioning of fixed assets:

Full instructions on how to correctly fill out and draw up the Inventory Book in 1C 8.3 can be found in the same report. To do this, use the More button. When this button is pressed, an additional menu opens with functions, when selected, you can add, change the report plate itself in order to make it convenient to work with it.

So, select the Help function:

We open it and get instructions for creating an inventory book:

There are two ways to create an inventory book in 1C 8.3. To do this, open the Select settings button on the report panel:

Select a specific department:

Indicate the person who is financially responsible for this unit for the safety of the fixed assets:

We form an inventory book for the desired period (month, quarter, year):

There is another possibility of filling out the inventory book in 1C 8.3 - choosing the person who is responsible for the information in this book:

All personal data of the person (full name), personnel number are recorded on the title page of the inventory book:

In order not to perform the Select settings function each time, there is a function in this report - Save settings. We select the required setting and with the Save button we fix the desired setting in 1C 8.3:

You can study the features of reflecting operations for accounting for fixed assets in 1C 8.3 (basic documents, accounting accounts, cost formation and depreciation in accounting records and accounting records) on the module.

When the fixed asset is put into operation, an inventory number must be assigned. What are the nuances, see our video tutorial:

Rate this article:

The creation and execution of inventory cards for accounting for an item of fixed assets in the OS-6 form is usually carried out at those enterprises and organizations that own a significant amount of property and which need to control its maintenance, storage and movement. For each individual fixed asset, its own card is issued, while cards can be entered both for company property and for leased property.

FILES

Before opening the card

Before creating this accounting document, it is necessary to draw up an act of acceptance and transfer of fixed assets - it is from it that information about the object enters the card. In addition, to fill it out, data is taken from other accompanying papers, such as, for example, technical passports of products, equipment and machinery.

The inventory card refers to the internal accounting documentation of the enterprise and information is entered into it during any actions with the property registered in it (acquisition, transfer from one department to another, repair, reconstruction, modernization, write-off, etc.).

Document registration rules

The inventory card of the object has a unified form with the OS-6 code, approved by the Decree of the State Statistics Committee of Russia dated January 21, 2003 N 7.

The document is drawn up for each object separately and in a single copy, while if the accounting of cards is kept in electronic form, then there must be a copy of it on paper (it is the paper versions that contain the “live” signature of the materially responsible person). It is not necessary to certify the document with the seal of the company, because. it refers to its internal documentation.

An example of registration of an inventory card in the form of OS-6

Filling in the document header

At the beginning of the document enter:

- the name of the company that owns the fixed asset,

- the structural unit to which the property is assigned,

- inventory number,

- the date of its compilation,

- the name of the registered object.

Here, in the column on the right, the enterprise code according to OKPO (All-Russian Classifier of Enterprises and Organizations) is indicated - it is contained in the constituent papers and the code of the fixed asset object according to OKOF (All-Russian Classifier of Fixed Assets). Continuing to fill in the right column, enter detailed information about the object:

- the number of the depreciation group to which it belongs according to the accounting of the enterprise,

- passport registration number,

- factory and inventory numbers,

- date of registration of the fixed asset for accounting,

- number of the account (sub-account) on which it passes.

Below, the location of the fixed asset object is entered in the corresponding lines (with the division code, if such coding is used at the enterprise) and information about the manufacturer (these data can be found in the data sheet).

Filling out the detail tables

The second part of the document opens the sections devoted to the registered object.

Note: information is entered in the first section only if the property was already used at the time of entering it into the card. If it is new, this section does not need to be completed.

In the second section the cost of the object at the time of acceptance for accounting and its useful life are entered.

Third section is issued during the revaluation of a fixed asset - and the price can vary both upwards and downwards. The difference between the original cost and after the revaluation is determined as the replacement price.

In the fourth section cards, information is entered on all movements of registered property. The data is entered here strictly on the basis of the accompanying papers indicating the type of operation, the structural unit to which the OS belongs, the residual value and information about the responsible person.

If the fixed asset is owned by several persons, then they must be indicated under the fourth table with the percentage distribution of shares.

Completing sections of the reverse side of the OS-6 form

In the fifth section indicates all changes in the original value of the object, regardless of the actions performed with it. The type of operation, data from the supporting document, as well as the amount of expenses incurred by the organization in the process of carrying out the necessary procedures are written here.

sixth section includes information on repair costs, with a full breakdown of each operation performed (type of repair, accompanying documentation, amount of expenses).

Seventh section contains special data on the item of fixed assets, including data on the content of precious and semi-precious metals, stones and materials in its composition.

In the last card table structural components, elements and other features that are a distinctive feature of the property, as well as its qualitative and quantitative indicators, are registered. If there are any notes, they are entered in the last column of the table.

At the end, the document is certified by the employee responsible for maintaining inventory cards at the enterprise (his position must be indicated here and his signature with a transcript must be affixed).

OS accounting is carried out according to inventory cards, which are entered for each object. In this article, we will look at:

- where to find the OS inventory card in 1C;

- how to create it;

- how to print an inventory card in 1C 8.3.

The organization must approve the form of an inventory card for further accounting of fixed assets. In 1C 8.3, the OS-6 form card is used. It reflects all operations carried out with the OS object from the moment it was accepted into the OS (clause 12, clause 13 of the Guidelines for OS accounting, approved by Order of the Ministry of Finance of the Russian Federation of October 13, 2003 N 91n).

Where can I find the OS inventory card (OS-6) in 1C 8.3? The fixed asset card in 1C 8.3 is located in the section.

An inventory card is entered when an organization enters. In general, the card is filled in automatically when posting documents, but some data must be entered manually.

The data in the fields filled in automatically are relevant for the current date. If you analyze (print out) past data, then in the field Information date enter the desired date.

If you do not see such a field in the card, then add it by clicking the button More - Reshape.

How to print an inventory card in 1C 8.3

Click the button Inventory card (OS-6) or More - Inventory card (OS-6) in the fixed asset card (section Directories - Fixed assets and intangible assets - Fixed assets).

The OS Inventory card form in OS-6 form will be filled in with relevant data on Date of information .

The inventory card must be updated when:

- moving the OS

- changing the accounting parameters of fixed assets;

- during modernization, repair (reconstruction, etc.);

- upon departure.

In 1C, you can also print an inventory book for accounting for fixed assets (form OS-6b), used to account for OS objects of a small business.

Report OS inventory book located in the section Fixed assets and intangible assets - Reports - Inventory book of fixed assets (OS-6b).